March 11, 2024

Market Commentary

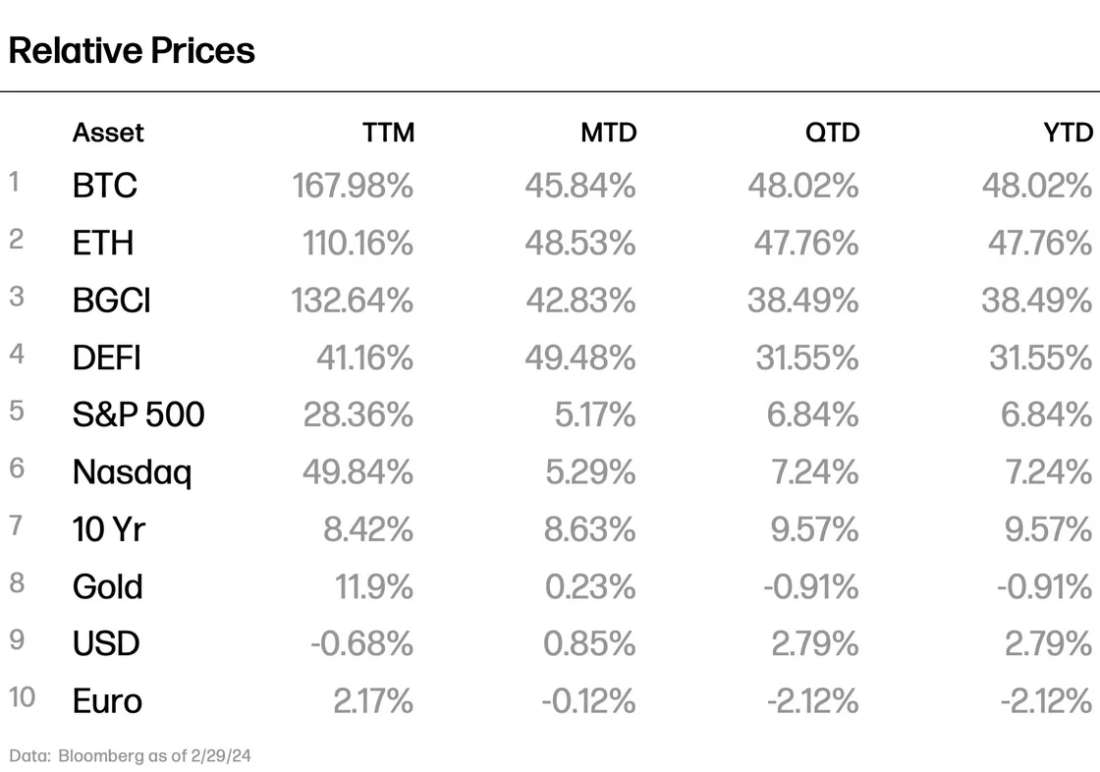

The late February rally brought renewed optimism to the crypto industry with blue-chip assets BTC and ETH surging (+45.84% and +48.53%, respectively) and the Bloomberg Galaxy Crypto Index trailing (+42.83%). The last week of February also brought a near-record for weekly inflows into digital asset investment products, with flows exceeding $1.8B. Weekly trading volumes for these products also surpassed previous highs, reaching $30B on the same week.

February saw bitcoin recapture $60,000, touching price levels not seen since November 2021. Bitcoin’s strong performance this past month, its best month over month performance since December 2020, had it within 10% of all-time highs. Despite these numbers being unfathomable to even the most bullish investors a year ago, Galaxy’s Head of Research Alex Thorn believes we have further room to run. Catalysts include the steady mass inflows into the U.S. spot BTC ETFs, the resurgence in futures open interest, the significant number of long-term bitcoin holders, and retail interest is starting to return to the market with Coinbase consumer trading volume up to 16% of the last market peak.

Augmented by spot BTC ETF inflows, bitcoin rose as high as $64,000 in February. Over the course of the last month, the newly minted spot BTC ETFs cumulatively brought in $8.7B and collectively topped $20B in AUM since inception. While spot bitcoin ETFs collectively hold a 1% share of the alternatives ETF market, bitcoin ETFs constituted 12% of the category’s monthly flows in a clear sign of outsized investor interest. February also saw bitcoin realize its largest monthly candle in its history, increasing its value in the year’s shortest month by +$18,000. The last time BTC’s price grew in a similar magnitude, October 2021, it proceeded to reach new all-time highs in the following month.

The bullish sentiments could be felt across the market as MicroStrategy extended its large bitcoin allocation with another buy of 3,000 BTC and Reddit disclosed that it had invested reserves into BTC in a SEC filing. With bitcoin’s recent price accumulation, MicroStrategy’s BTC holdings surpassed $12B, its highest recorded value. Further, Fidelity Canada recommending a 1-3% BTC allocation in its All-in-One Conservative ETF showcases the growing institutional belief in the role bitcoin can play in a portfolio. In an additional sign of the expanding institutional interest, Carson Group, a $30B RIA platform, approved multiple spot BTC ETFs, and Morgan Stanley announced that its Europe Opportunity Fund can now offer exposure to spot bitcoin ETFs. With bitcoin’s anticipated next halving less than fifty days away, it is likely bitcoin’s adoption among a new class of institutional clients is just beginning.

With bitcoin’s rapid price accumulation garnering the majority of mainstream crypto headlines, the second largest cryptocurrency by market cap is refusing to quietly play second fiddle. With its own stellar performance in February, ETH retested values not seen since right before the Terra-Luna collapse in May 2022. In the final week of February, Ethereum-themed digital asset investment products broke the prior record for weekly inflows. From a technical standpoint, the Ethereum network finalized its ultimate testnet before the Dencun upgrade is activated on the mainet. The Dencun upgrade, which is targeting a mid-March timeline, intends to improve Ethereum’s scalability through proto-danksharding (a feature seeking to make the network more scalable by efficiently processing large blocks of data). While large month-over-month gains, new recent highs in weekly flows, and continued successful progression to the network’s next upgrade should be regarded as catalysts for Ethereum, investors can still take a forward-looking approach with the smart contract-focused cryptocurrency as the AUM in Ethereum investment products remains 62% off highs at month end.

In February Coinbase announced its Q4 earnings, posting its first quarterly net profit since 2021. Coinbase’s transaction revenue bolstered its profitability push, as this metric grew 80+% QoQ in a strong indicator of resurgent investor interest. Similar to equities, crypto is very much in a risk-on regime with the altcoins that had standout performance in the past month belonging to more speculative subsectors such as AI-related tokens. Ignited by Meta and Nvidia’s promising earnings, AI tokens saw significant monthly gains with Bittensor (TAO) +32.01%, Render (RNDR) +74.46%, and Fetch.ai (FET) +150.49%. In prior cycles, the rotation from blue chip assets, such as BTC and ETH, into altcoins typically confirms the return of a bull market and silences the doubters and skeptics. As tends to happen during periods of frequent market activity, the increased focus on altcoins has also resulted in additional desire for stablecoins. Since stablecoins typically serve as one half of a trading pair for many cryptocurrencies, comparable amounts of funds flowing into stablecoins ($7.7B) since the January 11 ETF launch date as the newly minty ETFs themselves ($7.5B) is a harbinger of the trading demand across the entire digital assets ecosystem. With the calendar turning and spring approaching, it appears likely that we are not only leaving behind this winter but also the latest crypto winter.

Portfolio Considerations

As seen in the early stages of a bull market, the altcoin space followed the blue chips tokens’ recent price rally, and we are seeing developments in technology and increased interest from different market segments. February was a busy period for numerous scaling protocols with new developments, airdrops, and fresh investments into the space. Starknet, an L2 ZK roll-up secured by STARK validity proofs, announced the airdrop of Starknet Tokens (STRK) to the community, with over 700 million STRK estimated to be claimed by more than 1.3 million eligible addresses. STRK is intended primarily for network fee payments and governance participation. This airdrop event was notable for its broad distribution and marked as one of the widest distributions. The STRK airdrop also rewarded early Ethereum stakers pre-Merge, setting a precedent for future airdrops to more generously reward Ethereum-aligned contributors. STRK's pre-launch perpetual futures were trading at $1.80 on the decentralized futures platform Aevo before soaring to $5 on centralized exchanges immediately after release.

Another spotlighted scaling solution is EigenLayer, which has seen its total value locked (TVL) surge to $10B, up from a $1.1B valuation earlier in the year. This growth underscores its expanding influence within the decentralized finance (DeFi) sector. The protocol facilitates users' deposit and restaking of ETH through various liquid staking tokens to enhance the security of third-party networks. EigenLayer's TVL experienced a significant five-fold increase from $2B at the start of the last month, thanks to the removal of token restaking restrictions and TVL caps for each token. In February, other well-known and established scaling solutions such as Optimism (OP) and Arbitrum (ARB) also saw price increases, further highlighting the market's interest in and the importance of scaling solutions for prominent Layer 1 blockchains.

In the DeFi space, Uniswap's governance token, UNI, experienced a 60% price surge following a proposal by the Uniswap Foundation to overhaul the governance system and encourage active participation by rewarding UNI token holders who stake and delegate their tokens. This marks a significant departure from previous initiatives, aimed at improving governance and reward mechanisms within Uniswap, the largest decentralized exchange by volume. The proposal was unanimously accepted by the community.

Institutional Adoption Highlights

Crypto Performance and Volatility Data